Happy Halloween! Ready for a real scare? Check out how much longer it’s taking to sell property now compared to last year. Yikes!

Also, this week we’re going to address the two big questions I’m getting from clients:

- Should I buy, sell or hold?

- If not now, when’s the right time to make a move?

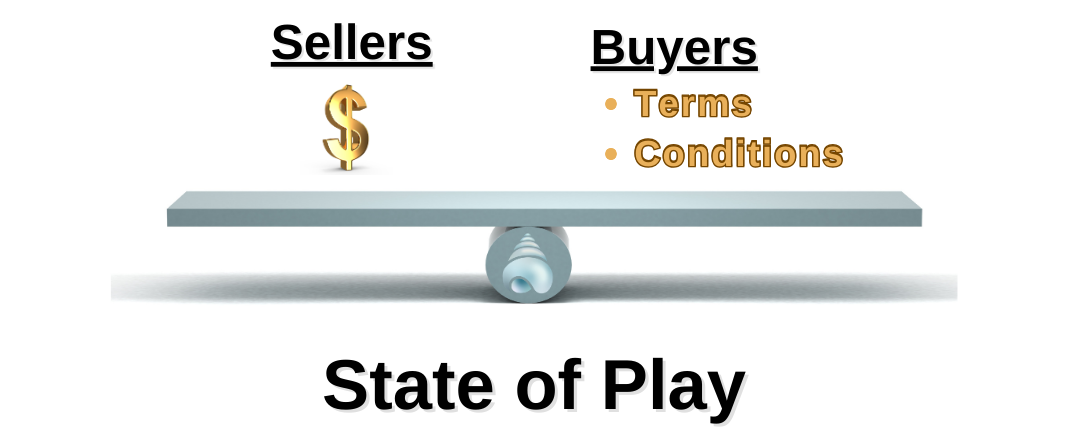

The current State of Florida’s Real Estate Market.

I would say right now, it’s balanced: sellers are holding firm on prices (for now), while buyers are securing some concessions—like favorable terms and conditions—that they haven’t seen in a while.

So, when should you buy or sell? I believe significant price movement won’t happen until mortgage rates drop below 6%. When that happens though, expect both transactions and prices to jump—quickly.

We’ll dive deeper into my forecast, but first, let’s look at what’s happening now, starting with Days on Market.

When Should You Buy or Sell?

I believe significant price movement won’t happen until mortgage rates drop below 6%. When that happens though, expect both transactions and prices to jump—quickly.

We’ll dive deeper into my forecast, but first, let’s look at what’s happening now, starting with Days on Market.

Emerald Coast Real Estate Market Update: Days On Market

FYI: 120-180 days on the market is considered a balanced market. Fewer days favors sellers and more generally favors buyers.

Year Over Year")

Red is this year – Blue is last year!

DOM Penalty:

Condos in the Destin area are taking nearly a month longer to sell this year compared to last. This “penalty” adds up quickly: that’s an extra month of mortgage payments, insurance, HOA dues, and more. Plus, in a softening market, which we’re seeing signs of, every day your property sits without an offer, its value is likely slipping.

What does this mean for sellers?

Make sure the Listing Specialist you hire has a proven track record of success—it matters now more than it has since the early 2000s.

Thinking of selling? Click to Get a FREE Value Analysis

Buying? Act Now and secure your place at the beach

Year Over Year")

DOM Penalty:

Homes in the Destin area are now taking 14 days (2 weeks) to sell—a solid timeframe compared to historical standards, but still almost two weeks longer than last year. That’s extra two weeks of mortgage, HOA, and insurance payments. Feel me here?

What does this mean for sellers?

The higher the Days on Market, the softer the market becomes, making it less likely for sellers to achieve top dollar. In short: higher Days on Market favors buyers. If you’re selling, choose your Listing Specialist wisely—it could mean tens of thousands of dollars.

Thinking of selling? Click to Get a FREE Value Analysis

Buying? Act Now and secure your place at the beach

To see how the days on market are changing in other areas of our Emerald Coast simply click on the link you’re interested in.

Destin Condo Sales

Destin Home Sales

30A Condo Sales

30A Home Sales

Panama City Beach Condo Sales

Panama City Beach Home Sales

Let’s get back to our big questions:

Should I Buy, Sell or Hold? Short Answer:

If you can achieve your goals for buying or selling now, then yes, you absolutely should. This helps you mitigate the risk of the market swinging in either direction—take the sure thing.

That’s good for buyers:

Can they dictate price? Maybe. We are seeing some softening in price but not much and I don’t expect this scenario to last long. Here’s why:

Supply and Demand:

There simply isn’t enough supply to fulfill demand- end of story. With too many buyers for too few properties, eventually prices are going to go up and they’ll likely grab their close friends – terms and conditions to come with them.

Bottom Line?

It’s a good time to be a buyer. Maybe not “great”, but the reality is, there may never be a “great” time again. As they say, the best time to buy is always five years ago. In 2030, you’ll wish you bought that beach property five years ago.

Want today’s best deals? Click here

Is it still a good time to sell?

Yes—if you can achieve your target price, it’s always a good time to sell. Trying to time the market is difficult and risky.

Key Signals to Watch For:

One clear indicator that prices are about to rise is transaction volume. When properties are actively changing hands, it signals a healthier market, and prices often trend upward.

So, when will transactions pick up?

Expect activity to pick up when mortgage rates fall below 6%. Check out the chart: rates above 6% make it challenging for buyers and investors to meet their financial goals, which reduces transaction volume. We saw this effect after the Great Recession (2006 – 2008), and it’s happening again now.

Big Question #2: If not now, when should I buy or sell?

For the beach real estate market to thrive, mortgage rates need to drop—plain and simple.

As the chart showed, when rates come down, more people can afford to buy homes and investment condos at the beach. And with affordable rates, investors return because the numbers start making sense again.

So, what could drive rates down?

Generally, it’s one or a combination of these three big factors:

- A Shift in Employment. Unfortunately, people have to lose jobs. Rising unemployment slows the economy, which puts pressure on the Fed to lower rates (quantitative easing) to stimulate business investment, construction, and hiring.

- The SPREAD between the 10 year T Bond and the 30 Yr Mortgage Rate needs to tighten.

Say what?

I’ll explain. Mortgage rates are heavily influenced by the gap (or “spread”) between the 10-year Treasury Bond rate and the 30-year mortgage rate.

Right now, this spread is sitting at an unusually high 2.5%. Typically, it ranges from 1.5% to 2% (you can see it on the graph – look at now compared to 2021). For mortgage rates to drop, we need this spread to tighten up.

Here’s Why It Matters?

When investors feel uncertain about the economy (like now), they move their money to safer investments, like 10-year U.S. Treasury bonds. This high demand lowers the Treasury’s yield (the interest paid on bonds).

But here’s the twist: it often raises mortgage rates. Why? Because banks are left holding “riskier” mortgages that investors might normally buy. To cover this risk, banks set higher mortgage rates.

What Needs to Change?

For mortgage rates to come down, we need more investors to see mortgage-backed securities (MBS) as attractive again. Once Treasury yields drop enough, MBS become more appealing, and investors start buying them again.

The Win for Us?

When banks can sell their mortgages to investors, they take on less risk. This lets them offer lower mortgage rates to buyers.

Bottom Line?

To get mortgage rates down, we need investors to view mortgage-backed securities as better investments than low-yield Treasury bonds. When banks can offload mortgages to investors, they can lower mortgage rates for buyers.

Thinking of selling? Click to Get a FREE Value Analysis

Buying? Act Now and secure your place at the beach

Ready for the Third Factor?

3. The Fed Policies

The Fed uses several tools to help reduce mortgage rates, here are two primary ones:

1. Simply Lowering the Federal Funds Rate

When the Fed lowers the federal funds rate (a process called “quantitative easing”), borrowing becomes cheaper across the board. This often leads to reductions in various rate-sensitive areas, most importantly for us – mortgage rates.

2. Buying Mortgage-Backed Securities (MBS)

Another powerful tool is the Fed’s buying of Mortgage-Backed Securities. When the Fed buys MBS from banks, it shifts the risk from the banks to the U.S. Treasury. This has several effects:

- Increases Liquidity: With risk reduced, banks have more cash to lend and can offer lower mortgage rates since they don’t need to price in as much risk.

- Stimulates Business Investment: The lower borrowing costs encourage businesses to invest in growth—building infrastructure, buying equipment, and hiring workers.

- Boosts Investor Confidence: As economic growth strengthens, investors are more willing to buy MBS, which further reduces mortgage rates.

The Result? Lower Mortgage Rates.

That’s the how. Now, when are rates coming down? Depends.

-

Unemployment Rate: If unemployment starts rising, the Fed may consider lowering rates to stimulate job growth.

-

Consumer Price Index (CPI): When inflation begins to fall, the Fed could lower rates to encourage more spending.

-

Fed Chairman’s Statements: Listen closely to what Jerome Powell says after the next Fed meeting (November 6-7). He may hint at their direction.

The Takeaway?

As long as unemployment stays low and inflation is steady, I don’t expect mortgage rates to drop anytime soon.

- 6")

Final Thoughts

Committed to your success,

John Moran – CEO

The Smart Beach Investor | Keller Williams Realty AT THE BEACH TEAM

We Make Real Estate Easy